The UN Climate Change Conference of the Parties (COP26) in Glasgow Officially Digging Grave for Coal-Fired Power Plants (CFFPs)

The COP26 summit held in Glasgow, Scotland of the United Kingdom on 31 October – 13 November 2021 has brought the parties together to accelerate action towards the goals of the Paris Agreement and the United Nations (“UN”) Framework Convention on Climate Change. For nearly three decades, the UN has been bringing together almost every country for global climate summits. By that time, climate change has shifted from a fringe to a global priority issue, in which CFFPs play a major role in causing the problem.

Back in 2015 when the Paris Agreement was born, the Parties to the Paris Agreement agreed to set out ambitious climate actions to limit global warming to below 1.5 degrees known as Nationally Determined Contributions (“NDCs”). Indonesia as a party member has set an NDC of 29% for an unconditional scheme (business as usual) or 41% with international support. However, according to the Minister of Environment and Forestry of Indonesia, in 2020 Indonesia failed to achieve the NDC target. Therefore, at COP26, acceleration and more efforts need to be made to turn the table, for that the Coal Pledge was born.

A. Coal Pledge – Countries and Banks Stop Financing Coal Industry

Under the Coal Pledge, the signatories agreed to commit to ending all investment in new CFFPs domestically and internationally. More than 40 countries have committed to phase out coal and switch to clean energy, including Indonesia. Several major banks also signed up to the pledge, agreeing to stop financing the coal industry. However, some of the world’s biggest coal-dependent countries, including China and the United States, did not sign up.

Indonesia as a signatory to the pledge has committed to phase out CFFPs by 2040 and start decommissioning a quarter of its coal capacity by 2030. While some have welcomed the move, others note that Indonesia’s commitment is so riddled that it makes the effort essentially useless. Particularly, Indonesia gives a second life for the coal industry through coal gasification i.e., the 0% royalty provision under Law Number 11 of 2020 on Job Creation Law. Coal gasification yields a clear-burning fuel, but the production process is even more carbon-intensive than just burning coal.

In addition, many questions arise on the pledge, one of which is related to the fact that none of these pledge commitments are legally binding – is there any big stick to force countries to commit to their pledge?

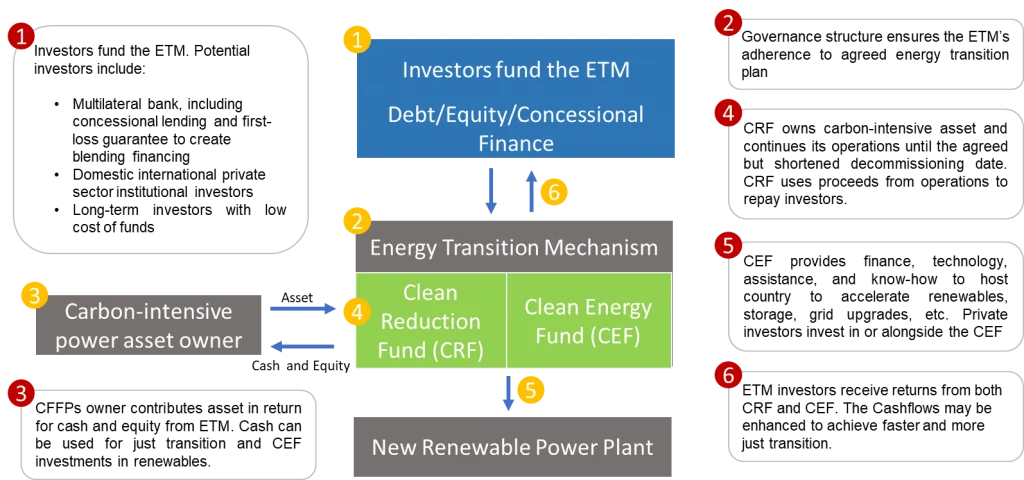

B. Energy Transition Mechanism (“ETM”) – Just and Affordable Transition

ETM is a blended financial partnership with developing country members. To aid in the battle against climate change, ETM is a ground-breaking initiative that will accelerate the transition from coal to clean energy. In order to bring clean energy to light, existing CFFPs, the biggest emission contributors, must retire early. ETM has a role to provide financial support in order to repurpose or retire CFFPs.

In an effort to cut in subsequent global warming and catch up with the NDC targets in the Paris Agreement, Indonesia has entered into a partnership agreement with Asian Development Bank (“ADB”) for ETM. This mechanism is expected to provide facilities that significantly shorten the life of legacy CFFPs. While reducing existing emissions from existing power plants, at the same time it is advisable to build renewable energy facilities to fulfill the demands.

C. ETM – Financing Portion and Mechanism Specifically in Indonesia

Based on the draft of ETM, blended financing consists of 2 financing portions. One portion is aimed at early closing or accelerating the transfer of functions of CFFPs. While doing so, another portion focuses on investing in generation, storage, and grid upgrading for new clean energy.

The following is mechanism of ETM of how it would operate:

While some have welcomed the scheme, others are concerned about the involvement of investors and CFFP developers, as well as the potential electricity consumers who will be forced to bear the additional cost of this plan. The lack of opportunities for the public and civil society to be involved in the formulation of the ETM should be brought to light.

Further, Ministry of State-Owned Enterprises (“SOE”) has enacted Regulation Number 3 of 2021 concerning Procedures for Write-Off and Transfers of SOE Fixed Asset which stipulates that transfer of state assets are possible, under at least one of the following conditions:

- No longer profitable;

- There are more profitable alternatives;

- For public interest;

- Part of restructuring program;

- Required by government agencies; or

- The only source of funding for urgent matters.

Asset transfer to private must use bidding mechanism. Direct appointment scheme will be allowed, only following two unsuccessful biddings.

D. ETM in Indonesia – Current PPA Makes it Costly

Considering that PPAs are the only revenue source for Independent Power Producer (“IPP”), State Electricity Company (Perusahaan Listrik Negara – “PLN”) is required to ‘take-or-pay’ any excess supply with 100% demand risk borne by PLN. Given the country’s investment risk, the guarantee of supply purchase is mandatory for the full contract length in order to make PPA bankable, as the IPP bears the fixed cost for plants to continue to operate and stand-by. As a result of take-or-pay scheme, the PPA is structured in a way that the IPP is guaranteed PLN will continue to pay the IPP even if they cannot distribute electricity for any reason.

According the authors opinion, considering the above element with incoming initiation of ETM, the take-or-pay scheme becomes irrelevant. As the ETM will began and IPP could not produce electricity, PLN should not guarantee to pay IPP even if they cannot distribute electricity for any reason. Therefore, addendum of this matters would be needful.

E. CFFP Key Consideration in Valuation

In order to identify the value of CFFP, the following key consideration shall apply:

- Review of historical financial and operating performance

Concerning regarding tariff amounts and earning to cover expenses, Industry trends and outlook – including trends of levels contracted capacity. Capital structure and investment of the CFFP, and track record of existing sponsors. - Study of existing revenue and cost structures

Study of valuation shall review regarding the existing Power Purchase Agreement (“PPA”) covering: tariff structure, tenor (5 to 35 years), probability of renewal upon expiry, and pass-through expenses. On the other hand-looking an outlook on wholesale electricity market prices and/or direct PPA tenors (if available), and the critical consideration regarding useful life of the plant. - Economic assumptions

Assumptions on exchange rate, inflation rate, and interest rate trends.

Related with the above, other key considerations that need to take into account are age and operations of CFFP, and government regulations and policy.

F. ETM – Where Are We and What’s Next?

In November 2021, ADB recently completed a pre-feasibility study that included financial and technical analysis in three pilot countries – Indonesia, the Philippines, and Vietnam. Currently, a full feasibility study is underway to determine the financial structure of the ETM, identify coal plant candidates for inclusion in the pilot program, and design just transition activities. In 10 – 15 years ahead, ETM targets to close 50% of CFFPs in Indonesia.

At the COP26 summit in Glasgow, Sri Mulyani expressed that the Indonesian government had identified 5,5gigawatt (GW) CFFPs to be early retired in the near term. For that, it requires about US$ 25 – 30 billion, which is expected to be covered by ETM. Considering Indonesia as a developing country, retirement or repurpose of CFFPs is expected not to overburden the State Revenue and Expenditure Budget. As of the time of writing, there is no further official information on the initial steps planning of the ETM.

G. A Glance at Carbon Trading and Carbon Tax Provisions Under Indonesian Regulation

In an effort to achieve the NDC targets of the Paris Agreement and in line with Indonesia’s commitment in COP26, the Indonesian government provides a Carbon Economic Value (“CEV”) regulatory instrument consisting of carbon trading and tax-carbon provisions regulated under Presidential Regulation Number 98 of 2021 concerning Implementation of CEV to Achieve National Contribution Target and Control of Greenhouse Gases in National Development (“PR 98/2021”). Article 47 stipulates that the implementation of carbon pricing can be conducted through several mechanisms, as follows:

- carbon trading;

- result-based payment;

- carbon tax;

In order to secure the development and new method of carbon pricing, the Minister of Environment and Forestry has the right to determine other mechanisms other than the above.

H. Carbon Trading Under Indonesian Regulation

Based on PR 98/2021, carbon trading is a market-based process of buying and selling permits and credits that allow a company or other entity to emit a certain amount of emission powered by the government, the business world, and the community through domestic and foreign trade. The main goals are to gradually reduce overall carbon emissions and reduce the contribution to climate change in NDC.

Further, carbon trading activities carried out inside and outside the country must comply with the Indonesian National Standard and obtain a Greenhouse Gas Emissions Reduction Certificate (GHG-ERC) issued through the national emission reduction mechanism. The carbon trading procedure consists of direct trading mechanism and offset mechanism, the implementing regulations of which are currently in progress.

I . Carbon Tax– Subject, Mechanism, Rate

The carbon tax is regulated under Article 13 of Law Number 7 of 2021 on Harmonization of Tax Regulations (“Law 7/2021”), which will be imposed on individuals or entities that purchase goods containing carbon and/or carry out activities that produce a certain amount of carbon emissions for a certain period.

The imposition of carbon tax will be carried out with a focus on two schemes i.e., the carbon tax scheme and the carbon trade scheme. In the carbon trade scheme, an entity that produces emissions exceeding the cap is required to purchase an emission permit certificate from another entity that produces emissions below the cap. On the other hand, entities can also purchase emission reduction certificates. If the entity is unable to purchase the certificate of emissions, the cap and tax scheme will apply.

In general, the carbon tax provision will be effective on 1 April 2022. As stated in Article 17 of Law 7/2021, this provision will first be imposed on entities that are engaged in CFFPs at a rate of Rp.30,00 per kilogram of carbon dioxide equivalent or equivalent units. If there is a situation where the price of carbon in the carbon market is lower than Rp.30,00 per kilogram of carbon dioxide, the minimum of Rp.30,00 is set. Taxpayers that actively participate in the carbon tax program are entitled to carbon tax reduction facilities and/or other treatments to help meet their carbon tax obligations.

J. Conclusion – Early Retirement, What About Remaining Reserve?

In line with the development and transition to renewable energy, Indonesia has set out a roadmap and partnership with ADB to encourage early retirement of 50% of the CFFPs by 2040 with a just and affordable mechanism. In addition, Indonesia has signed the Coal Pledge and committed to both phase out CFFPs by 2040 and no longer establish new CFFPs. Considering Indonesia as a country dependant on CFFPs, a big question arises, is there a big stick to force Indonesia to commit to their pledge, and what about the remaining coal reserve in the meantime until 2040?

***

ADCO Law earns the trust to represent clients from multinational companies to emerging entities across a wide range of industries to achieve their business objectives in Indonesia.

ADCO Law as a Law Firm in Jakarta assists the clients to structure, organize and implement their business ventures and investments, including structuring, financing, and securing investments as well as establishing new foreign companies in Indonesia.

Should you have more queries regarding this matter, please do not hesitate to contact us.

ADCO Law

Setiabudi Building 2, 2nd Floor, Suite 205C

Jl. H.R. Rasuna Said Kav. 62, Setiabudi Karet

Jakarta Selatan, 12920, Indonesia.

Phone : +6221 520 3034

Fax : +6221 520 3035

Email : info@adcolaw.com

Disclaimer: This article has been prepared for scientific reading and marketing purposes only from ADCO Law. Accordingly, all the writings contained herein do not constitute the formal legal opinion of ADCO Law. Therefore, ADCO Law should be held harmless of and/or cannot be held responsible for anything performed by entities who use this writing outside the purposes of ADCO Law.